When you have located the property you wish to purchase you will most likely present an offer to purchase through a licensed realtor. Contracts prepared by a realtor must provide a three-day attorney review period, during which either party may review the proposed contract with their respective attorney. During such review the contract may be approved, disapproved or approved with changes. It is in your interest to discuss the contract with your attorney during the three-day review period so that your attorney may more effectively represent your particular concerns.

Since most purchases of residential real estate include the provision that a that the purchasers primary duty is to immediately, efficiently and aggressively pursue such mortgage financing. As a practical matter, that means an application for mortgage financing must be completed immediately following attorney review, if not before, with a mortgage company previously chosen by the applicant. Typically, mortgage contingency purchaser will need mortgage financing to complete the purchase, it is important to note periods run between thirty and sixty days. Although this office will assist you in perfecting your mortgage application by dealing directly with the mortgage company, it is the purchaser’s primary responsibility to keep in contact with their mortgage banker or broker to ensure the completion of the mortgage application itself and to satisfy any subsequent conditions that the mortgage company imposes on the commitment. THE COMMITMENT IS AN EXTREMELY IMPORTANT DOCUMENT. YOU MUST CAREFULLY READ YOUR COMMITMENT IN ORDER TO UNDERSTAND WHAT IS REQUIRED OF YOU FOLLOWING THE ISSUANCE OF THE WRITTEN COMMITMENT AND BEFORE CLOSING OF TITLE.

Residential real estate contracts call for the purchaser, at his own expense, to conduct an inspection of the premises in order to determine the existence of any latent or non-apparent deficiencies in the property. It is extremely important that you keep our office informed of the status of all contingencies contained in your contract of sale including termite inspection, structural inspection, well and septic inspections and radon inspection It is vital that these inspections be completed and a written report received within the time period set forth in the contract. Please arrange to have the inspection company forward to your attorney copies of all relevant inspections as soon as they are prepared. Upon your receipt of the results of these inspections, contact your attorney to discuss any problems revealed by the inspections. Your attorney will assist you in negotiating with the Seller to resolve any such deficiencies.

When obtaining mortgage financing it is required that a title search and a title insurance policy be obtained in at least the amount of your mortgage. This office is responsible for ordering same for you. Most banks require a new survey of the premises at the time of closing.

Once you have received your mortgage commitment and this office has received the title search and survey, this office will comply with your bank’s instruction and submit all documentation they require for review prior to closing. After the bank’s review of the documentation, they will allow us to schedule a closing at which time we will contact you, the Seller’s attorney and the real estate broker and arrange for a mutually convenient closing date and time. Immediately following your receipt of a mortgage commitment, you should make arrangements to obtain an ORIGINAL homeowner’s insurance policy NOT BINDER (hazard insurance) along with an ORIGINAL paid receipt of the first year’s premium.

The date of the closing on the contract is an estimated closing date and should be used as a rough guideline. Please do not plan on closing on this particular date, as that is not always possible. On the afternoon immediately prior to the actual closing, our office will prepare the final figures in consultation with both the mortgage company and the opposing attorney. Once this calculation has been completed, our office will contact you with the exact amount of money you should bring to the closing to cover the remaining down payment and any closing costs attendant to the closing. Our office will give you a bottom line figure that will include the amount due to the Seller along with these closing expenses.

Closing costs are all of the costs associated with processing the paperwork to buy a house. When you make an offer on a home, your real estate broker will put your earnest money (deposit) into an escrow account. If the offer is accepted, your earnest money (deposit) will be applied to the down payment or closing costs. If your offer is not accepted, your money will be returned to you. The amount of your deposit varies. The more money you can put into your down payment, the lower your mortgage payments will be. Some types of loans require 10-20% of the purchase price. Closing costs – which you will pay at closing – average 3-4% of the price of your home. These costs cover various fees your lender charges and other processing expenses. When you apply for your loan, your lender will give you an estimate of the closing costs, so you won’t be caught by surprise.

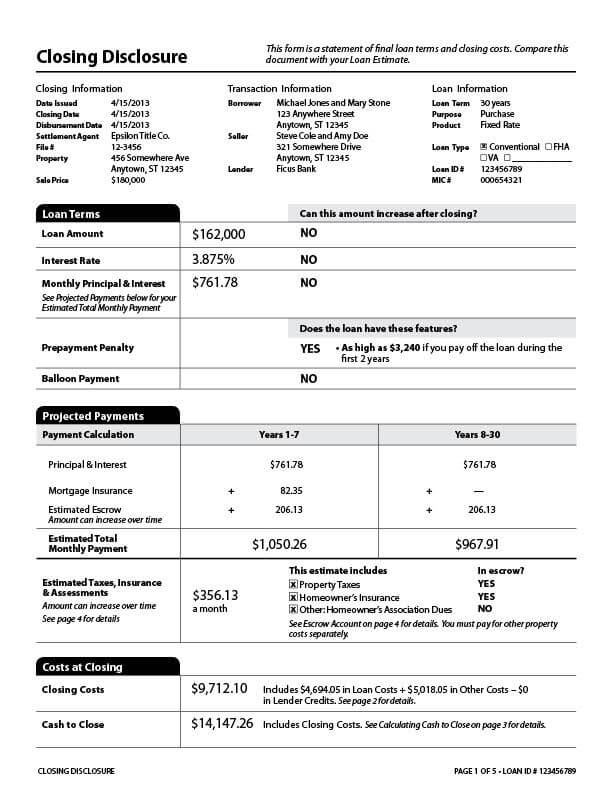

At least three days before your closing, you should receive a Closing Disclosure, which is a five-page document that gives you more details about your loan, its key terms, and how much you are paying in fees and other costs to get your mortgage and buy your home.

Many of the costs you pay at closing are set by the decisions you made when you were shopping for a mortgage. Charges shown under “services you can shop for” may increase at closing, but generally by no more than 10 percent of the costs listed on your final Loan Estimate.

Page 1: Information, loan terms, projected payments costs at closing

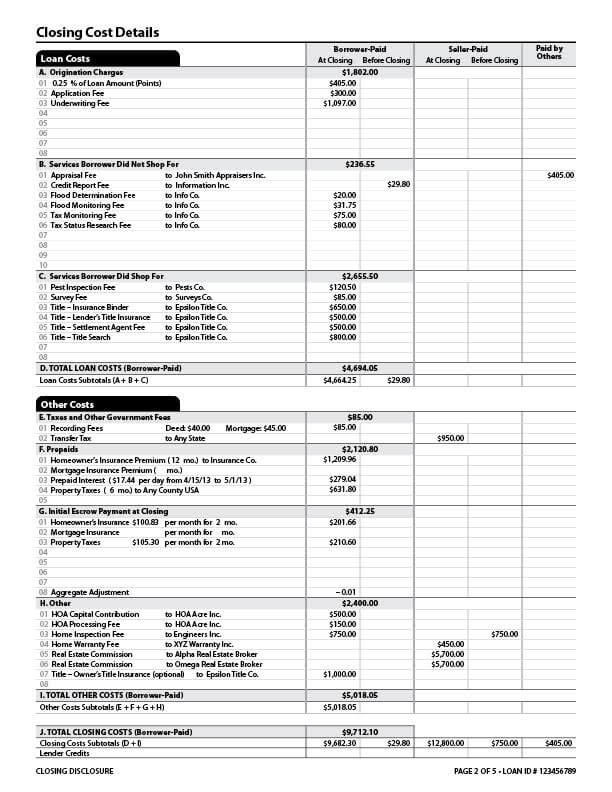

Page 2: Closing cost details including loan costs and other costs

Loan and other cost details paper

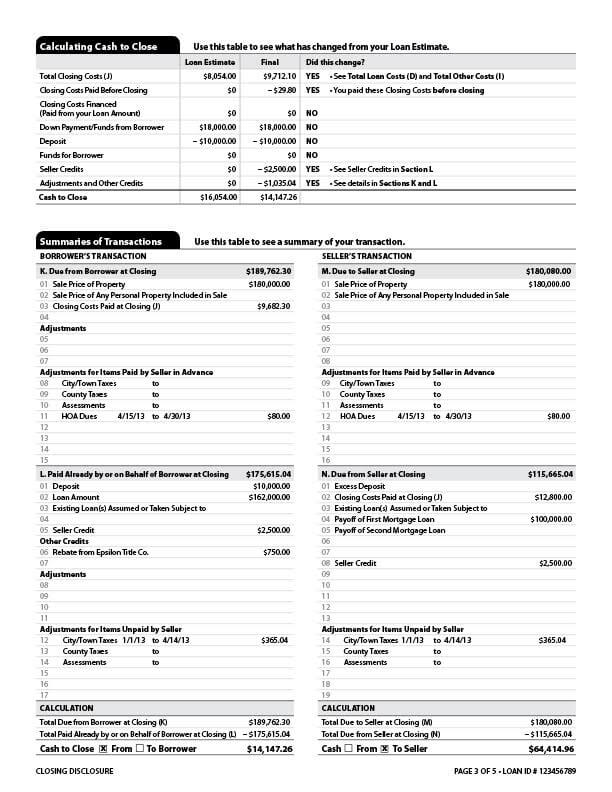

Page 3: Cash needed to close and a summary of the transaction

Summaries of transactions

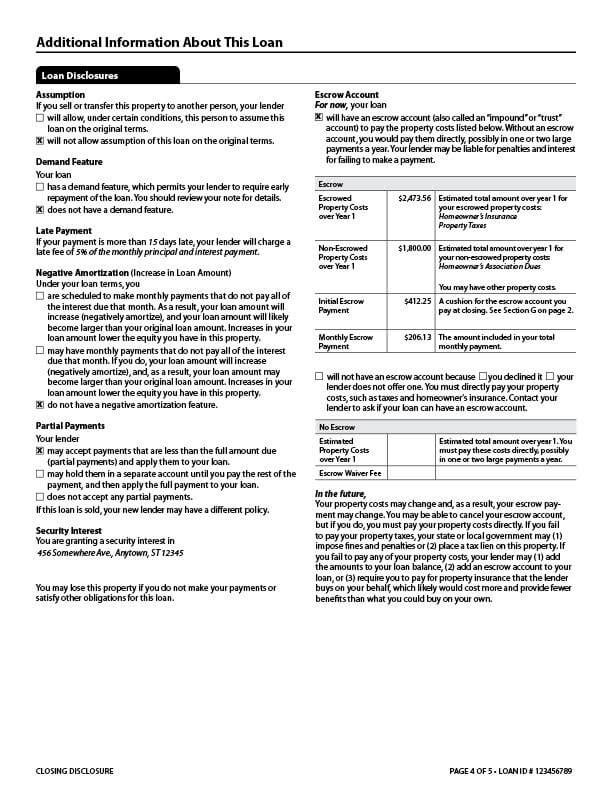

Page 4: Additional information about your loan

Real Estate Loan disclosure paper

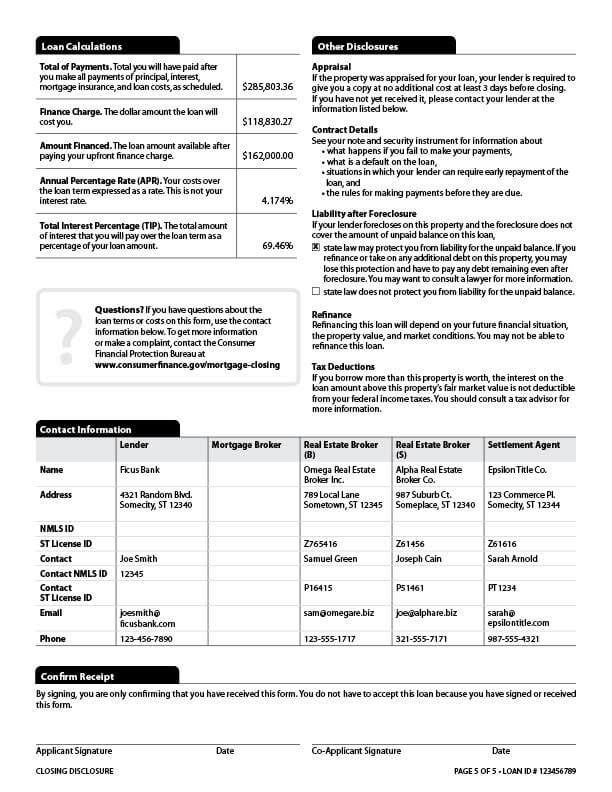

Page 5: Loan calculations, disclosure information and contact information

Real Estate Loan Calculations and other disclosures